BlackRock Case: What Every Tax Professional Should Know

Borys Ulanenko

This is a summary of the UK First-tier Tribunal (Tax

Chamber) decision on BlackRock HoldCo 5 LLC and The Commissioners for

Her Majesty’s Revenue and Customs (HMRC) published on November 3, 2020.

The case refers to the 2009 deal between BlackRock Group

and Barclays Global Investors (BGI). The deal included the

purchase of Barclays exchange-traded fund business, iShares. You may even own

some of these exchange-traded fund shares, as they are among the most popular

ETFs on the market!

In 2009, New York-based BlackRock agreed to pay $13.5

billion to acquire London-based Barclays' investment management business. The

transfer pricing dispute between BlackRock and HMRC, though, is around how

BlackRock structured this transaction. The structure of the deal involved

intra-group loan notes, which was subject to debate.

BlackRock Group requested advice from

external consultants (EY) on how to arrange a potential acquisition transaction.

The advice was not just focused on tax risks and optimization considerations

but also on commercial and regulatory factors. The financial industry is highly

regulated, and therefore the deal had to comply with rules and regulations both

in the UK and the US.

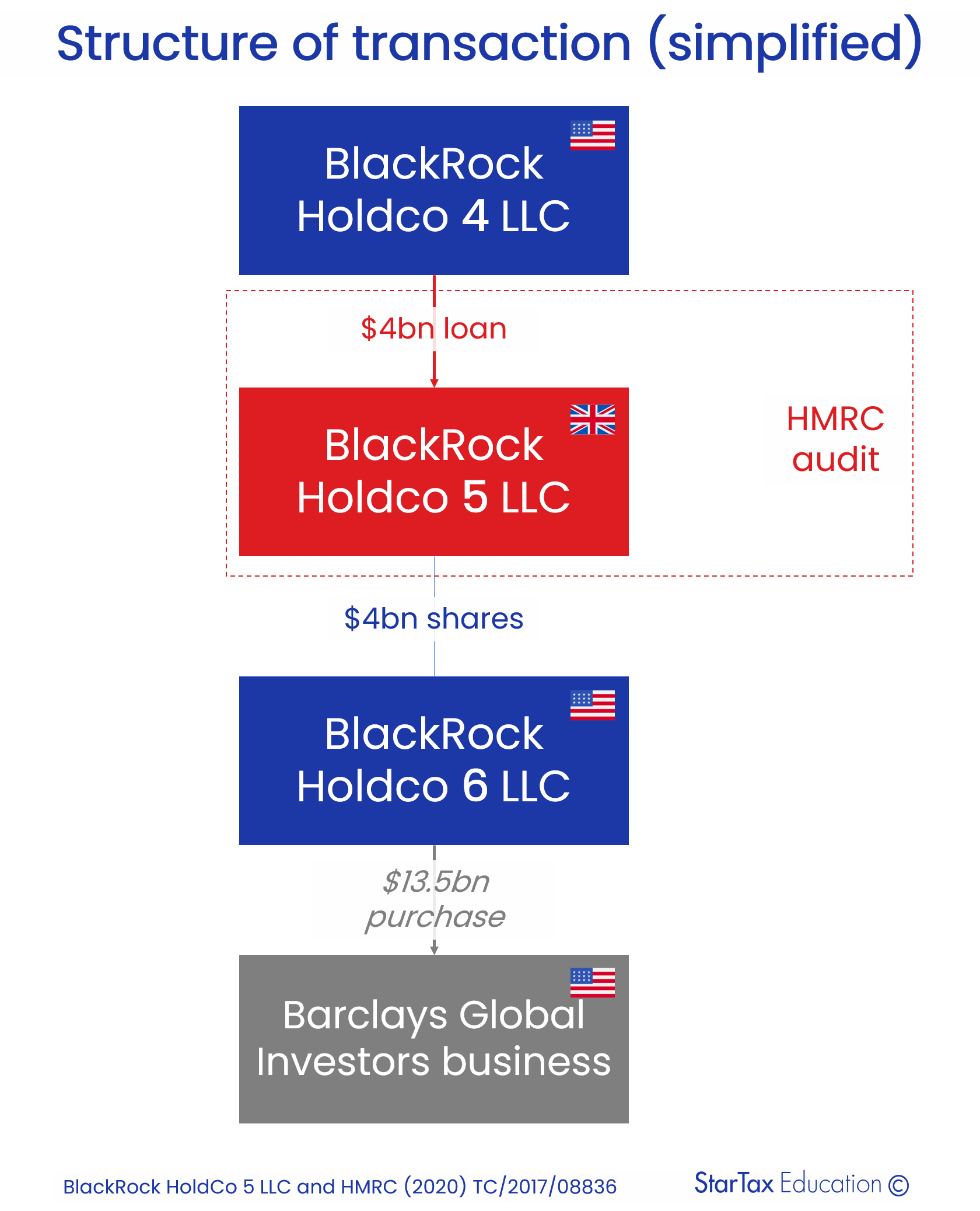

Ultimately, BlackRock Group decided to structure the

acquisition by arranging several holding companies. These entities were

registered in the State of Delaware (the US). At the same time, the company

that received an intra-group loan (BlackRock HoldCo 5 LLC) was resident in the

UK, based on the fact that the place of central management and control of BlackRock

HoldCo 5 LLC was in the UK. In one of the emails, the structure used by

BlackRock Group was called a “US/UK Sandwich.” The deal structure involved providing

the intra-group loan (via issuing loan notes) to UK-resident BlackRock HoldCo 5 LLC.

From the facts of the case, it appears that the main purpose of adding

the UK resident to otherwise wholly US structure was to ensure that potential

changes to the US “check the box” regulations will not lead to significant

adverse US tax consequences.

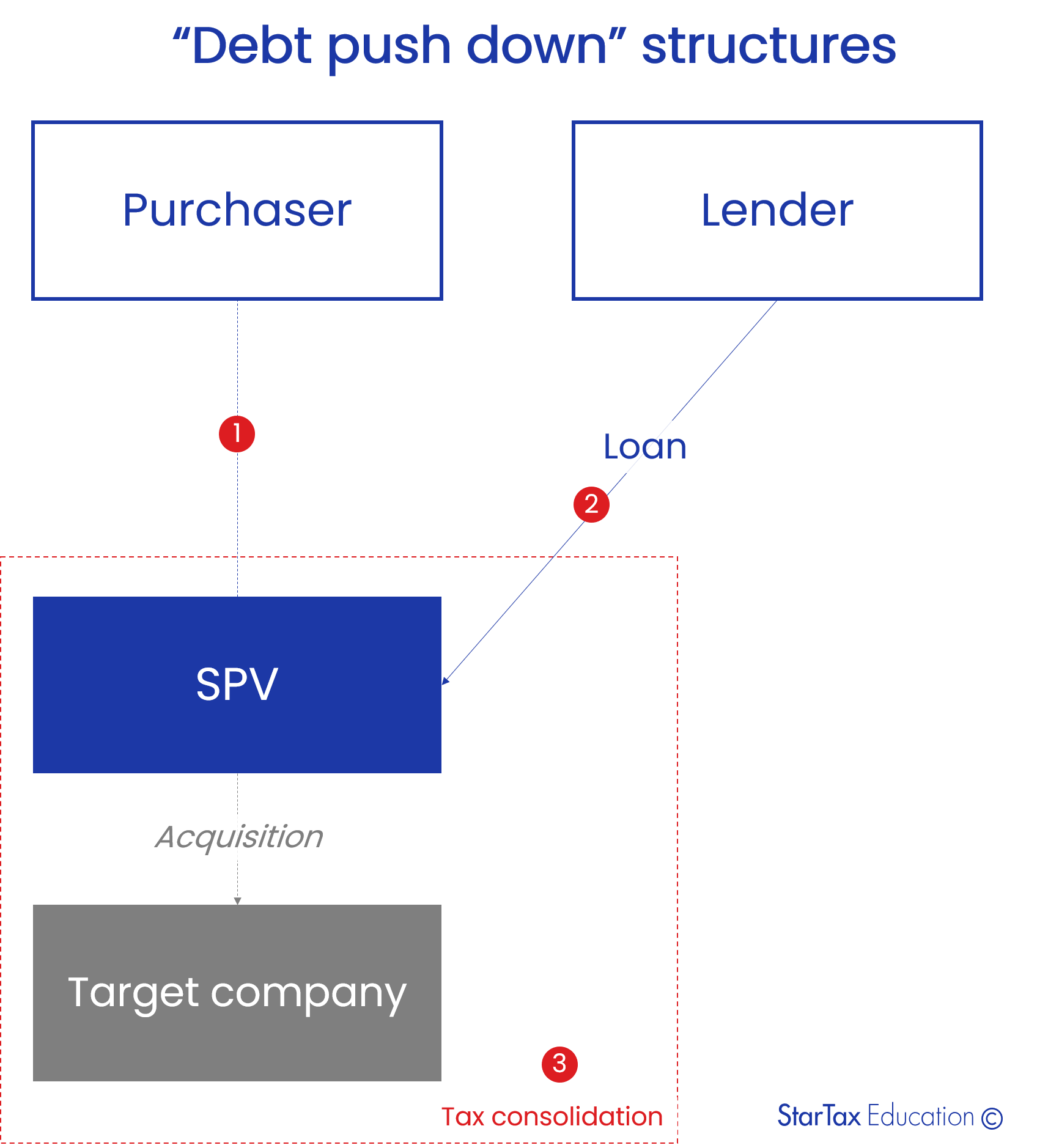

Another consideration (that ultimately did not prevail but was also

discussed by BlackRock tax team with EY advisors) was “debt push-down”

possibility.

Debt push-down: a simple example (for educational purposes)

Purchaser establishes a new special purpose vehicle (SPV, an entity created for a particular defined purpose) in the target company's country.

Another group’s company (often parent/treasury company) provides an intercompany loan to SPV for the acquisition.

Debt is “pushed-down” using tax consolidation(tax grouping, fiscal unity) in the country of SPV/target company.

As a result, the interest deductions in SPV offset the profits of the target company.

Transactions under review and dispute points

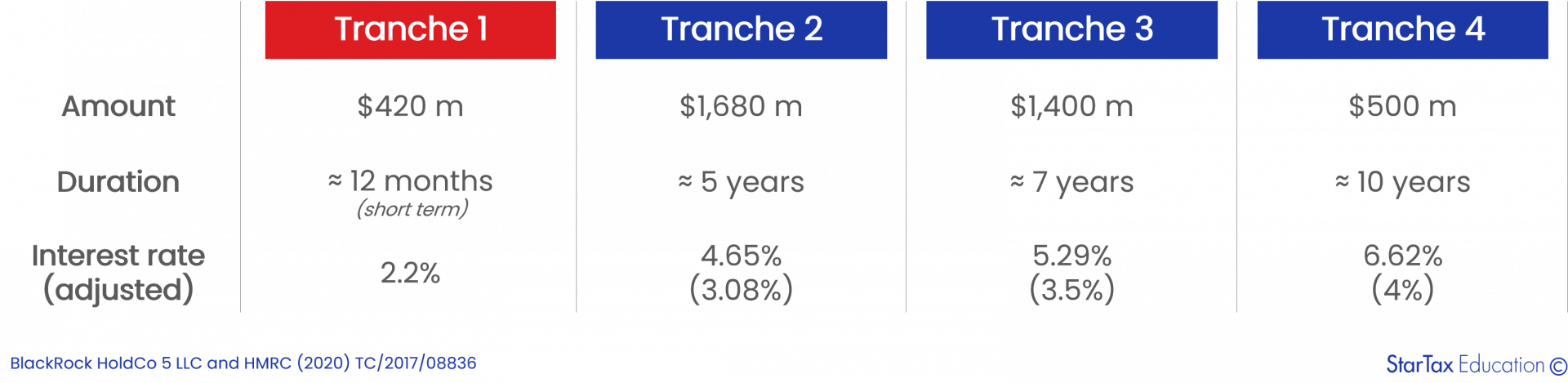

To fund the acquisition, BlackRock HoldCo 5 LLC issued

loan

notes for approx. US$4bn to the parent company to finance the investment. There

were four tranches with fixed interest rates (that were later adjusted

downwards):

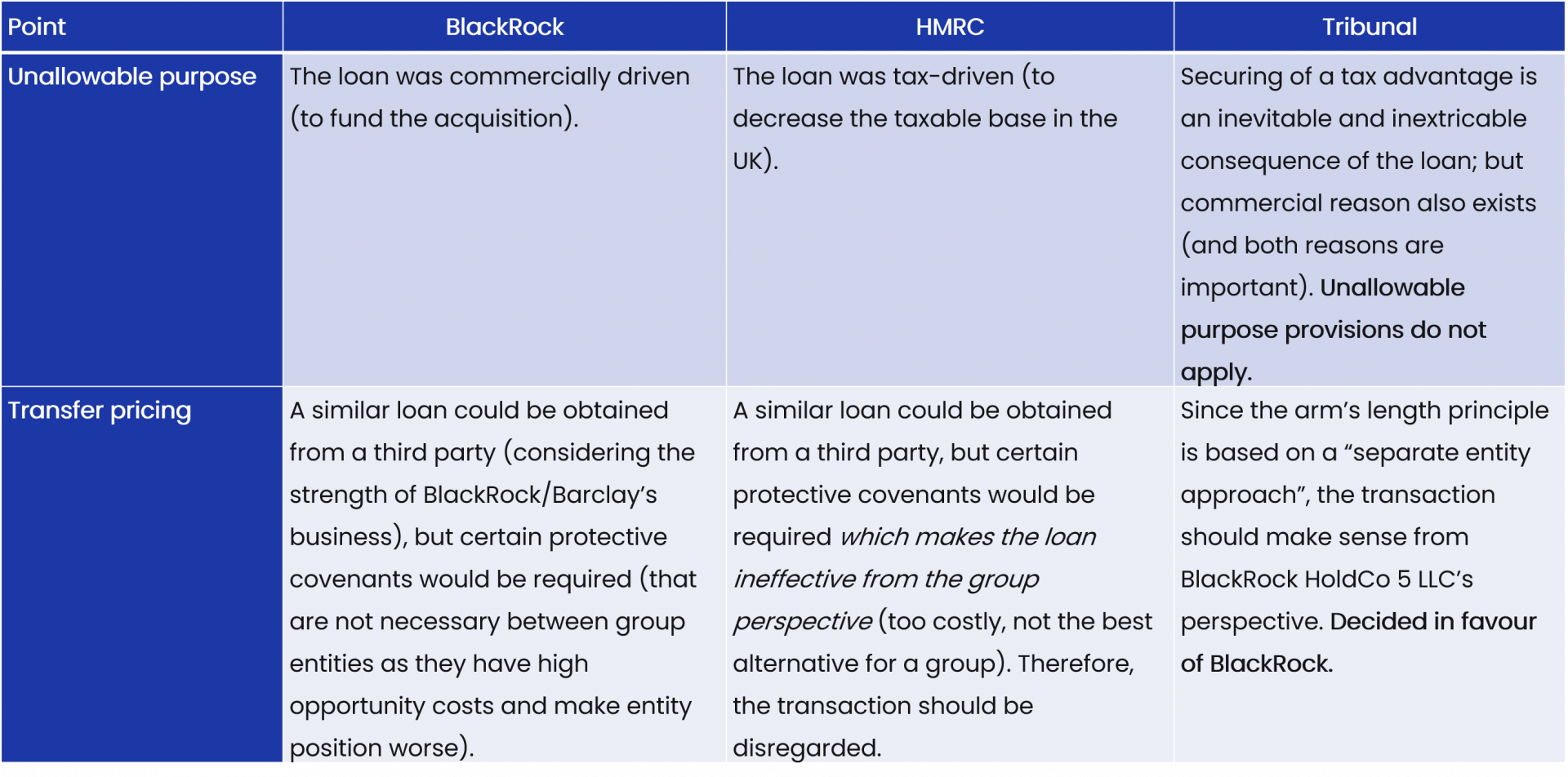

HMRC challenged the loan from two positions: stating that the loan was tax-driven (“unallowable purpose” issue), and whether the transaction would have happened if it had taken place between independent companies (“transfer pricing” issue). The table below summarizes the positions of the taxpayer, HMRC, and the Tribunal.

Conclusions

There are several important takeaways from this case:

Economic substance and residence test are critical. When BlackRock HoldCo 5 LLC had to make important decisions on loan and acquisition, BlackRock’s tax team insisted on board meetings to be held in the UK (and even rescheduled the meeting to accommodate one of the directors). If BlackRock had not taken all precautionary matters, the position would be much weaker.

Transfer pricing does not always focus on the price (or interest rate), but also considers the transaction itself. The first question raised in the court was if parties had been independent, would they have entered into the loans at all?

In essence, the case was won thanks to strong tax function in 2009, not good lawyers in 2020. We have seen a lot of recent cases where heavy investment in litigation experts and lawyers did not pay back, mainly because the background case was weak.

The EU is run by an elected EU Parliament and an appointed European Council. The European Parliament approves EU law, which is implemented through EU Directives drafted by the Commission. National governments are then responsible for implementing the Directive into their national laws. In other words, EU Directives are draft laws that then get passed by national governments and then implemented by institutions within the member states.

What is CbCR?

Country-by-Country Reporting (CbCR) is part of mandatory tax reporting for large multinationals. MNEs with combined revenue of 750 million euros (or more) have to provide an annual return called the CbC report, which breaks down key elements of the financial statements by jurisdiction. A CbC report provides local tax authorities visibility to revenue, income, tax paid and accrued, employment, capital, retained earnings, tangible assets and activities. CbCR was implemented in 2016 globally.

Created with

Login or sign up to start learningLogin to start learning