4 Key Rules Every Cost Contribution Arrangement Should Follow to be Defensible

Borys Ulanenko

A Cost Contribution Arrangement (CCA) is one of the common

frameworks for MNEs to develop and exploit intangibles and services. The

transfer pricing of CCAs is a complex topic that attracts considerable public

attention. Both the OECD Guidelines and the UN Manual have separate chapters

dedicated to CCAs. Also, some tax authorities have developed detailed guidance

and regulations on CCAs that provide useful insight into their approach.

The idea of a CCA in international tax is broadly similar to a Cost-Sharing

Arrangement (CSA) in the US. The major difference between two is that a CSA may

be arranged only for joint IP development, whereas a CCA may be organised for

joint IP development as well as service arrangements. In this chapter, we will

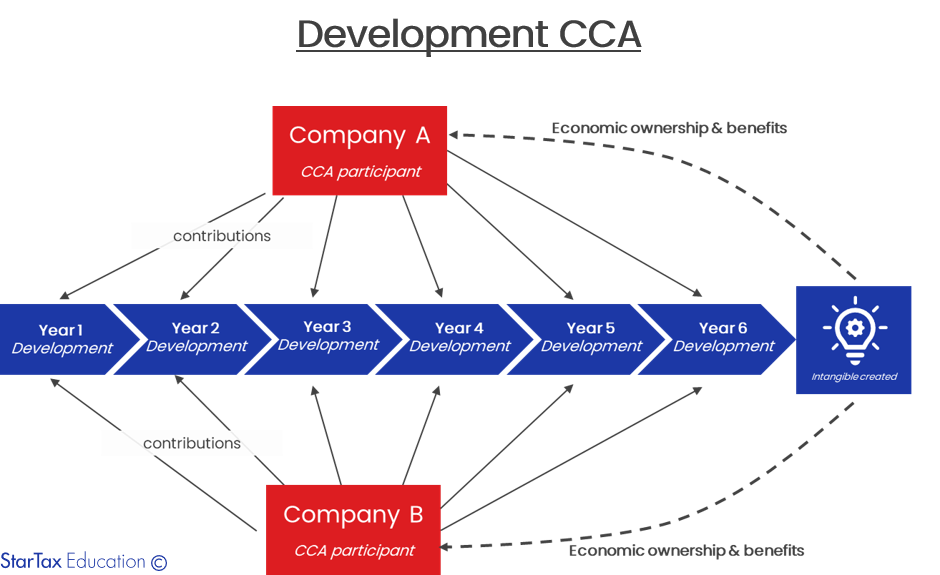

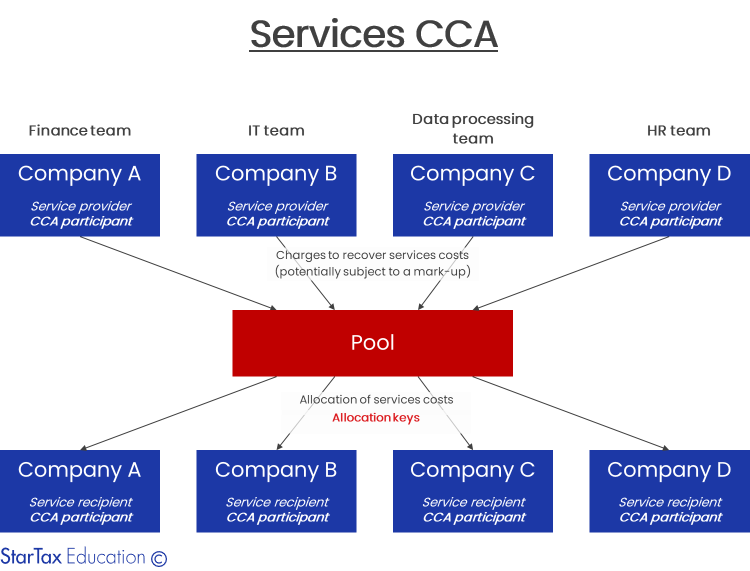

focus on CCAs (not CSAs). Diagrams below illustrate development and services CCA models:

There are several key rules that every CCA should follow to be defensible from transfer pricing and tax perspective:

A participant in a CCA should

have the reasonable expectation that he will benefit from the objectives

of the CCA activity itself (and not just from performing

part or all of the activity within the CCA). Thus, for example, where a CCA

is established with the objective of developing an intangible, a party that

carries out research activities but is not assigned an interest in the

intangible, will not be a participant within the CCA.

A participant’s proportionate share

of contributions to the CCA should be consistent with the proportionate share

of expected benefits that the participant reasonably expects to receive.

A

CCA should have necessary balancing payments, buy-in and buy-out mechanisms in

place.

CCA

documentation should be VERY strong. OECD Guidelines para. 8.52 provide the

list of necessary information every taxpayer should maintain to defend his CCA,

but you should also check your local recommendations and regulations (if they

exist).

What are

other CCA elements that are critically important from your perspective? Let us know,

and we will add them to the list! In our

textbook, we dedicate a detailed chapter for the discussion about CCAs, including

8 practical examples and cases that explain services and development CCAs.

For more details about the textbook and the course, contact us:

The EU is run by an elected EU Parliament and an appointed European Council. The European Parliament approves EU law, which is implemented through EU Directives drafted by the Commission. National governments are then responsible for implementing the Directive into their national laws. In other words, EU Directives are draft laws that then get passed by national governments and then implemented by institutions within the member states.

What is CbCR?

Country-by-Country Reporting (CbCR) is part of mandatory tax reporting for large multinationals. MNEs with combined revenue of 750 million euros (or more) have to provide an annual return called the CbC report, which breaks down key elements of the financial statements by jurisdiction. A CbC report provides local tax authorities visibility to revenue, income, tax paid and accrued, employment, capital, retained earnings, tangible assets and activities. CbCR was implemented in 2016 globally.

Created with

Login or sign up to start learningLogin to start learning