Glencore Case: What Every Tax Professional Should Know

Borys Ulanenko

This is a summary of the decision of the Federal Court of Australia on Commissioner of Taxation v Glencore Investment Pty Ltd [2020] dated 6 November 2020. It can be interesting for international tax and transfer pricing professionals, as it gives valuable details and the pricing of commodities, as well as interpretation of the arm’s length principle generally. For more details about the arm's length principle and commodities transactions, visit our transfer pricing course page.

Glencore

business model and transactions under review

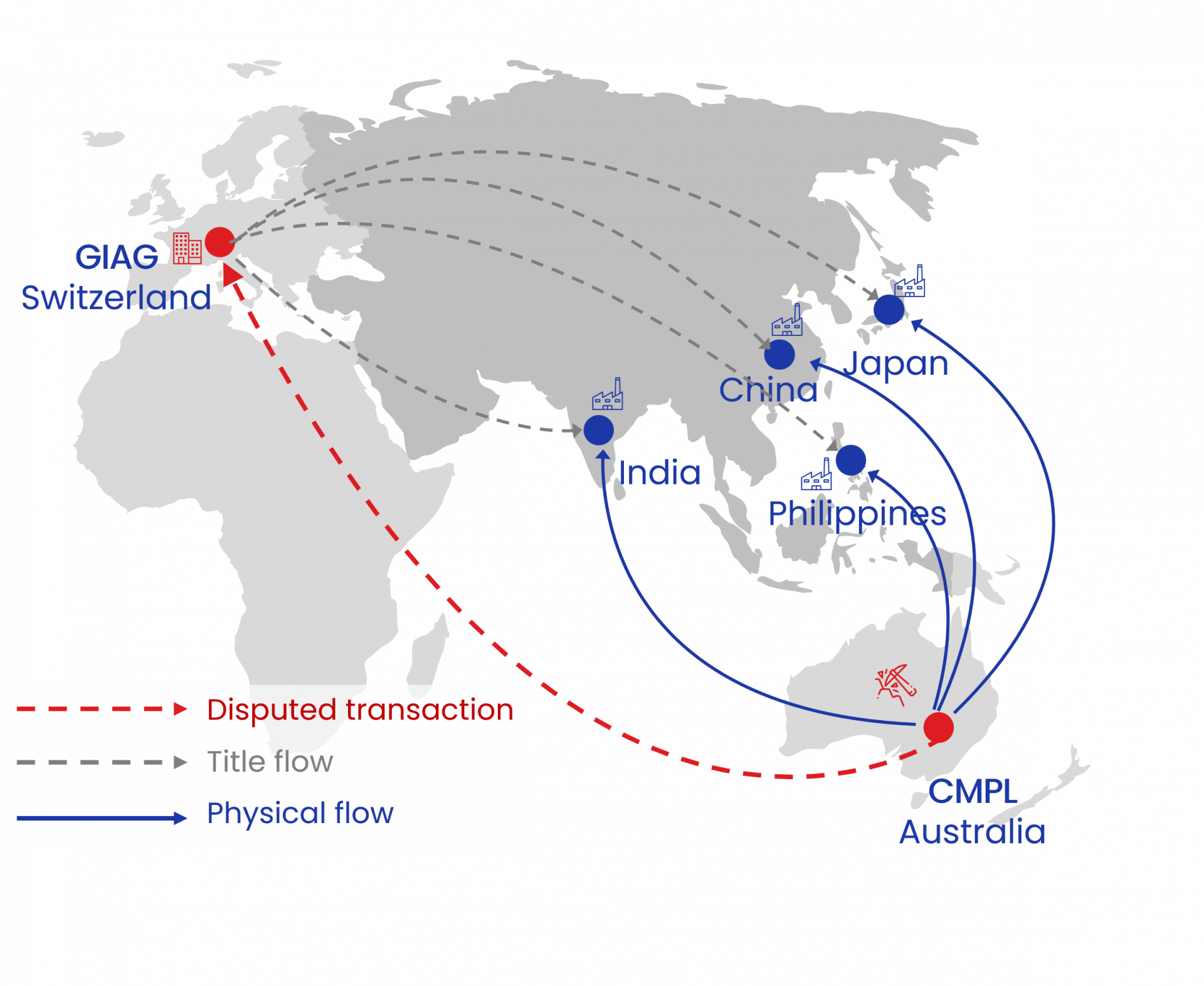

Cobar Management Pty Ltd (“CMPL”) is a resident of Australia and is a subsidiary of Glencore Group. CMPL owned and operated an underground copper mine at Cobar in central western New South Wales.

In 2004, CMPL entered into “offtake agreement” with Glencore International A.G. (“GIAG”), resident of Switzerland, for a sale of all cooper concentrate produced by CMPL to GIAG. GIAG was marketing and selling cooper concentrate globally (i.e. acted as a trader). Copper concentrate mined by CMPL was sold to independent smelters in India, China, Japan and the Philippines.

The

agreement included several important features:

It

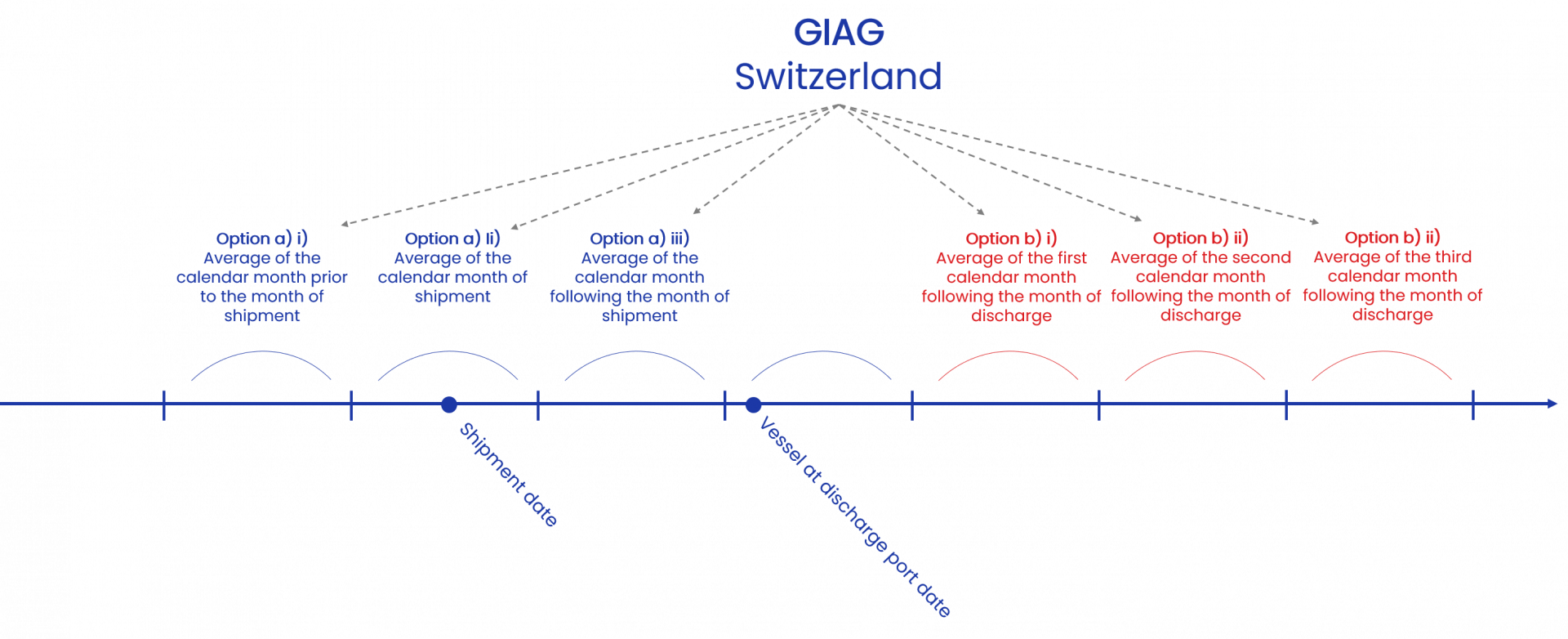

allowed significant quotational period optionality for GIAG. Offtake agreements

specify the period, whether a day, days, weeks or months, with which the price

or average price of the copper is to be ascertained. In the industry, this is known as the

“quotational period.” Some agreements

give the buyer options about how to choose the applicable quotational periods

and how often such choices can be made (“optionality”).

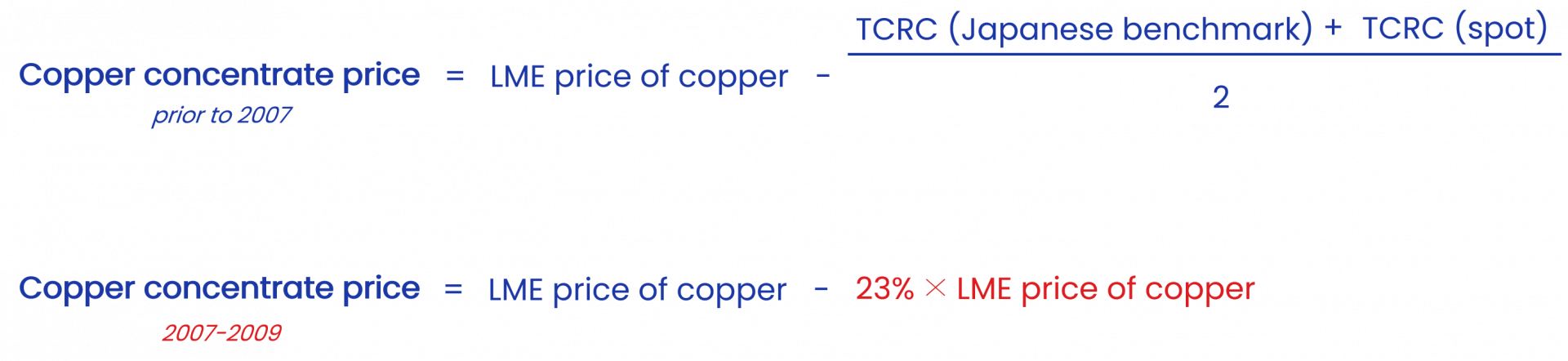

The

price of copper concentrate was calculated using a formula based on London

Metal Exchange copper price minus the cost to a smelter of treating and

refining the copper concentrate also referred as TCRCs (and some other, less

material, deductions). In other words, the price for copper concentrate is

based on the price of the final product (copper) produced from the concentrate,

minus the cost of independent manufacturers of copper that they will bear to make

that final product. Information about both material elements of the price is available

from trustful sources, though both are very volatile and not correlated.

The

agreement was significantly amended in 2007:

The

parties abandoned their reliance on benchmark TCRCs. They agreed to adopt a price sharing clause

instead, to determine the deduction to be made.

For the 2007 to 2009 years, TCRCs were set at 23% of the copper price.

The use of price sharing formulas is another way of establishing deductions in copper

concentrate sharing formulas, and they are often used in the market. An

advantage of this type of formula was that it eliminated a particular type of

dangerous volatility arising from the use of benchmark TCRCs, namely an inverse

movement in the price of copper and benchmark TCRCs which can occur from time

to time.

Even

greater “quotational period” optionality was given to GIAG (on shipment by

shipment basis)

The

previous clause that stipulated the freight allowance (“to be agreed annually”)

was replaced by a fixed US$60 per wet metric ton.

Dispute

points

ATO challenged

the intra-group pricing between CMPL and GIAG for years 2007-2009 on the following

basis:

Movement

from TCRC benchmark to price sharing arrangement made CMPL worse off

financially.

Such

a quotational period optionality gives significant benefit to the buyer (GIAG)

at the cost of the seller (CMPL) and allows the buyer to always realise a profit.

The

fixed freight allowance of US$60 is based on the cost of freight to India,

which is the most expensive (vs China, Japan and the Philippines). Therefore, where

copper concentrate was shipped to countries other than India, the freight

allowance paid by CMPL to GIAG was overstated.

Positions

and key arguments

Issue

Glencore

ATO

Court

Use

of price sharing arrangement (23%)

Standard

market mechanism, allows moving significant risks to the buyer (GIAG)

Move

from TCRC benchmark to price sharing arrangement made CMPL worse off

financially; 23% is overstated

Both TCRC benchmark and price sharing is arm’s length, the taxpayer is free to choose based on risk management strategy, ATO was not able to suggest an alternative to 23%. ATO position disregarded

Quotational

period optionality

Observed

in transactions between independent parties, therefore arm’s length

Gives

too much flexibility and protects the buyer from the downside risk; should be

compensated quid pro quo

Quid pro quo compensation is not calculated by ATO and is not substantiated. ATO position disregarded

Fixed

freight allowance

Did

not provide arguments

US$60

is too high

ATO position supported

Conclusion

Court

supported taxpayer in all material aspects of the case. Essential points

highlighted by the decision:

ATO

was allowed to challenge the pricing methodology and the price sharing

percentage, however, it failed to prove that the price sharing arrangement

itself is not arm’s length and failed to challenge 23% price sharing percentage.

·

Reconstruction

of the transaction (according to the OECD Guidelines) was not appropriate.

·

Taxpayers

can choose their own risk mitigation strategy and are not required to maximise

profitability at any cost.

Use

of forecasts and budgets is useful, but not sufficient (especially in volatile

markets). Use of hindsight should be avoided.

There were

several other interesting discussion points, and therefore we recommend reading

the case in full.

What was interesting for you in this case? Share it with us using contact details below.

For more details about the textbook and the course, contact us:

The EU is run by an elected EU Parliament and an appointed European Council. The European Parliament approves EU law, which is implemented through EU Directives drafted by the Commission. National governments are then responsible for implementing the Directive into their national laws. In other words, EU Directives are draft laws that then get passed by national governments and then implemented by institutions within the member states.

What is CbCR?

Country-by-Country Reporting (CbCR) is part of mandatory tax reporting for large multinationals. MNEs with combined revenue of 750 million euros (or more) have to provide an annual return called the CbC report, which breaks down key elements of the financial statements by jurisdiction. A CbC report provides local tax authorities visibility to revenue, income, tax paid and accrued, employment, capital, retained earnings, tangible assets and activities. CbCR was implemented in 2016 globally.

Created with

Login or sign up to start learningLogin to start learning